Irreparable damage is done to your credit rating when you experience a short sale or some of the other related possibilities– not as bad as foreclosure or bankruptcy, but are damaging nevertheless. However, most of the agencies and people of less repute will never take the trouble to tell you the far-reaching consequences of foreclosure or foreclosure on your credit standing.

Effect on Credit Score

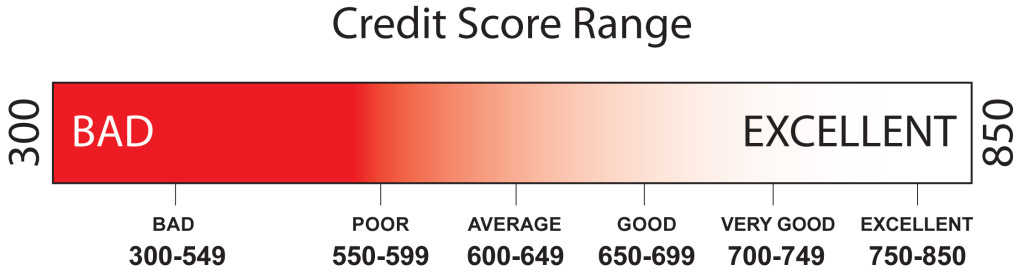

A foreclosure, as you would have sensed, can damage your credit rating for a long time. A foreclosure or a short sale can impact your credit standing for as much as 7 long years and also setting you back immediately by a whopping 200-300 points on your FICO credit score. A short sale of your property, as a response to avoiding foreclosure, can also cause your credit rating to drop considerably and can set you back about anywhere from 55 to 125 points on your FICO score – this might show up as “foreclosure arrangement”, or “debt settlement”. Additionally, a deed-in-lieu might just be as lethal as a foreclosure itself since it entails a transfer of ownership.

Foreclosure is always best avoided. It might allow you to stay rent free for a while until you will be asked to leave, but the negative consequences a foreclosure has on your credit rating – which implies that your ability to avail credit for important things like student loans and car loans etc is severely affected because that’s how severe FICO along with potential lenders take this event to be.

Tax Implications

Often overseen, but a critical aspect that should help you choose between a foreclosure or a short-sale, is the tax part of it all. IRS considers any discharged debt as an income and hence you will be taxed on that. For instance, if you declared bankruptcy due to foreclosure of a property worth $300,000, this debt which is now discharged by bankruptcy is considered income and you will now have to pay tax on that amount. A short sale, on the other hand, causes your debt to be forgiven – the difference between the mortgage amount and the amount the lender sold it for. This forgiven debt is also taxable.

Another aspect to consider when choosing a foreclosure vis-à-vis a short sale is how long a homeowner can wait before buying another home or being able to avail a new home loan. Most homeowners think that short sale will let them avail a new home loan in a short time period, which is unfortunately not the case. A set of guidelines from Fannie Mae, stipulate that individual home owners must wait out for at least 24 months before they would be considered for new home loans. It might also help to remember that in the event that the short sale generates much lesser an amount than the mortgage due, the lender can proceed to file a deficiency judgment which is like a thorn in the wound and something the homeowner has to battle with again.

Nothing is as easy as it might first sound and a homeowner must look into all possible options before settling with any one option. Hearsay and casual advice should never be paid attention to. Think creatively and take help from competent professionals to arrive at customized solutions that would bail you out of this problem fully. You might want to transfer ownership to an investor by signing a deed but bring your mortgage payments up to current from the proceeds that came from dissolving your equity. More such solutions are possible when you approach it the right way.